Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

3 HIGH TRAFFIC LOTS: ZONED C2

Each Lot = .32 Acres

Available Separately or Together

C2—Highway, Service, Commercial

Located across from Super 1 Foods

Hwy 53 area, Rathdrum

208-660-0518

Check it out at www.RealEstate-Browser.com

3 HIGH TRAFFIC LOTS: ZONED C2

Each Lot = .32 Acres

Available Separately or Together

C2—Highway, Service, Commercial

Located across from Super 1 Foods

Hwy 53 area, Rathdrum

208-660-0518

Check it out at www.RealEstate-Browser.com

Rustic Craftsman Elegance is articulated in an impressive list of posh amenities. This Single level residence on 2.4 Acres in Harbor View Estates incorporates nature’s finest materials: Granite Counters, Custom Knotty Alder woodwork & Cabinetry & stone rockwork throughout.

An exceptionally equipped Gourmet Kitchen is outfitted with an entire Suite of Upscale Appliances.

Other finery includes Walk-in Master Suite Steam Shower & 4+ Car Garage.

Outdoor grounds boast the same attention to excellence and detail with landscape curbing, lush lawn, colorful flora and a lovely mountain view.

Directions:

15 SCENIC MINUTES FROM COEUR D’ALENE

Highway 95 South, Left on KIDD ISLAND,

Right into HARBOR VIEW ESTATES, Left on MEADOW LANE

4545 Meadow Lane Drive, Coeur d'Alene

Call Christy Oetken of Windermere Coeur d’Alene Realty today:

Check it out at

http://www.realestate-browser.com/viewdetails.php?nid=77204&mls=11-3060

There you have it! USNews.com has discovered what the rest of us have known all along. This time, Post Falls has been recognized in the Top 10 Most Affordable Mountain Towns for Retirement. Below are excerpts from the full article:

10 Best Affordable Mountain Towns for Retirement

These places offer scenic views and groomed slopes at economical prices.

Posted: July 12, 2010

…To find this and other low-cost mountain towns, U.S. News fired up our Best Places to Retire search tool. We looked for places that offer access to plenty of skiing, trails, and wildlife, while still providing affordable housing and a reasonable cost of living. We also used the Onboard Informatics data to screen for other retiree-friendly characteristics, such as access to healthcare and a low crime rate…

Few aspiring retirees have enough saved to buy a retirement home in Aspen or Lake Tahoe. But if you’re willing to look beyond the most well-known ski resorts there are mountain towns that offer scenic views and well-groomed slopes at far more affordable prices. In Salt Lake City, the host city for the 2002 winter Olympics, the average home sale price has dropped by 11.92 percent since last year. And in Bend, Ore., average housing prices decreased by a whopping 17.62 percent since 2009. Redding, Calif. and Post Falls, Idaho have also experienced recent drops in average housing prices, which could mean bargains for newcomers. …

Check out these 10 affordable places to retire in the mountains:

Blacksburg, Va.

Bend, Ore.

Boone, N.C.

Bozeman, Mont.

Burlington, Vt.

Fayetteville, Ark.

Post Falls, Idaho

Redding, Ca.

Salt Lake City, Utah

HIGHLANDS GOLF COURSE AREA

Priced to SELL FAST!

Gas Fireplace & 3 Car Garage

LARGE HOME & HUGE SHOP

on 4.5 Acres

4 Beds, 3 Baths

3240 Sq Ft

LEATHERWOOD LOT 1 & LOT 2

Build your Custom Estate

Two 10 Acre Parcels available

Lake Newman, Mountain & Valley Views

GREAT INVESTMENT PROPERTY

1800 sq ft Duplex

2BR/1BA Units

Great Rental History

Visit Our website,

ALL of the listings on the Coeur d’Alene Multiple Listing Service

plus our

and

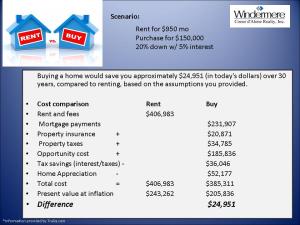

You might be surprised to find that a careful Cost/Benefit Analysis still favors BUYING, despite increasing interest rates. Here’s one scenario:

1. The cost of an alternative that must be forgone in order to pursue a certain action. Put another way, the benefits you could have received by taking an alternative action.2. The difference in return between a chosen investment and one that is necessarily passed up. Say you invest in a stock and it returns a paltry 2% over the year. In placing your money in the stock, you gave up the opportunity of another investment – say, a risk-free government bond yielding 6%. In this situation, your opportunity costs are 4% (6% – 2%).Investopedia explains Opportunity Cost

1. The opportunity cost of going to college is the moneyyou would have earned if you worked instead. On the one hand, you lose four years of salary while getting your degree; on the other hand, you hope to earn more during your career, thanks to your education, to offset the lost wages.Here’s another example: if a gardener decides to grow carrots, his or her opportunity cost is the alternative crop that might have been grown instead (potatoes, tomatoes, pumpkins, etc.).In both cases, a choice between two options must be made. It would be an easy decision if you knew the end outcome; however, the risk that you could achieve greater “benefits” (be they monetary or otherwise) with another option is the opportunity cost.

Dear Friends,

It’s probably no surprise that rising interest rates have a significant impact on your pocket book.

But how much of an impact? The True Cost may shock you!

Consider this:

The average stay in a home is 5 to 7 years

according to the National Association of Realtors®.

Knowing you like to stay informed, we have provided three real-world home buying scenarios in the graphics below. From these hypothetical comparisons, we hope you can get a better idea of the true cost of the interest rate hikes that are expected in the near future.

Assuming that you remain in your new home for 7 years, it is very clear the HUGE impact of rising interest rates.

WAITING TO BUY could cost you THOUSANDS of dollars!

(Visit our website to view larger PDF graphics of these three scenarios.)

Home “A” Costs $150,000

At the current interest rate of 4.875%, the monthly payment will be $797.

If you wait until the interest rate rises to 6%,

your monthly payment will increase by $85,

for a total annual increase of $1020!

If you stay in that home for 7 years,

you will be spending $7140 MORE!

Waiting to purchase this $250,000 home could cost you

$140 per month

$1680 per year

If you stay in that home for 7 years,

you will be spending $11,760 MORE!

Thinking of buying? Now is a great time, if you want to save $$ in your monthly budget, as well as over the life of your potential mortgage.

Are you waiting for a lower purchase price?

The “savings” of a few thousand dollars off the purchase price will actually COST you THOUSANDS when the interest rates rise.

Don’t wait to make your next Real Estate move.

Call Now

to take advantage of

High Inventory and Low Interest Rates!

As experienced REALTORS®, and long-time North Idaho residents, we can provide an impressive list of professionals whom we’ve come to trust over the years. With our expertise in guiding our clients through all kinds of Real Estate transactions, we are uniquely qualified to help you achieve your real estate goals in 2011!

We’ll help you navigate through every phase of the process.

Here’s a “sneak peek” at our Front Page Ad that will be published in tomorrow’s Coeur d’Alene Press.

Thinking of selling? We’re hard workers. Put us to work for you!

Call us for your FREE Comparative Market Analysis.

To see what your home, land, investment or commercial property is worth in today’s market, call

or

of

Windermere Coeur d’Alene Realty

We will work hard for YOU!

Visit our websites:

We just listed this beautiful home on the Coeur d’Alene River:

We just listed this beautiful home on the Coeur d’Alene River:

We hate to brag, but we can’t help but notice the noteworthy comparisons between this lovely property and its namesake, a beautiful National Park on the Emerald Isle:

The charming town of Killarney Ireland is situated in the southern region of County Kerry, snuggled between sparkling lakes, deep forests, and high peaks. County Kerry is famous for its mountain ranges, cliff-filled coastlines, and beguiling islands and peninsulas. Killarney, also called Cill Airne, serves as the bustling center of this gorgeous region. The town of Killarney itself is gracefully charming and the nearby Killarney National Park can’t be missed.

Like its namesake, this Killarney Road Riverfront Acreage is an idyllic place to call home. We can’t promise a pot of gold at the end of the rainbow, but we can promise vistas of golden pasture, amethyst river, emerald pines, and purple mountains. A rainbow of color!

Here are a few more of its amenities:

5+ Acres

(.71 Acre on the Coeur d’Alene River)

located near the Killarney Lake Boat Ramp & Dock

off Highway 3

Cedar-Sided 2 Bedroom Home

SHOP, Garden House & Guest Cabin

No need for the “Luck 0′ The Irish”

because this property is priced to sell…

And that’s NO BLARNEY!

Check it out at

www.RealEstate-Browser.com

or call

of Windermere Coeur d’Alene Realty

for more details.

A Ticklish icy splash…a mischievious winking flash…

tittering and giggling and skipping along the rocks on the water…

The West Fork of Pine Creek

gambols through this 6 acre natural wonderland.

Come and play!

Build your dream home on this buildable 6 Acre parcel.

Like to hunt, hike or sight-see? This parcel backs up to BLM land, too!

Call Randy Oetken

of Windermere Coeur d’Alene Realty for more details:

Check it out at www.RealEstate-Browser.com

First-time homebuyers almost always make a few mistakes when buying their home. Perhaps they pay too much, choose the wrong type of mortgage or neglect to budget for needed home improvements.

Working with a trustworthy, experienced lender can help prevent such mistakes. But consumers also need to take responsibility for their budgets and choices.

“Before buying a home, consumers need to develop a short- and long-term perspective on their purchase,” says Michael Harrison, area director for MetLife Home Loans in Southwest Ohio.

Following are the four biggest financial mistakes of first-time homebuyers:

Lenders qualify buyers based on their incomes and debt-to-income ratios without considering how much the borrowers spend on items such as transportation, savings, food and other necessities.

Lenders qualify buyers based on their incomes and debt-to-income ratios without considering how much the borrowers spend on items such as transportation, savings, food and other necessities.“A lot of first-time buyers are optimistic about the future and excited about buying a home, so they borrow the absolute maximum they can afford instead of allowing themselves wiggle room for a partial loss of income or for future expenses such as children,” Harrison says.

Financial experts recommend that consumers decide how much they want to spend each month on housing before meeting with a lender.

“Every buyer should create their own budget and know their limits,” says Stephen Adamo, president of Weichert Financial Services in Morris Plains, N.J.

Adamo says many first-time homebuyers experience a sizable change in their housing payments. Some new owners may go from $500 per month in rent to a monthly mortgage payment of $2,000, he says.

“You need to deal with payment shock,” Adamo says.

Not getting prequalified early enough

Meeting with a lender for a buyer consultation and prequalification for a mortgage should be the first step toward homeownership. Yet many first-time homebuyers wait until they are ready to start house hunting before contacting a lender.

While most consumers know it’s important to have a high credit score, not everyone understands how costly a low score can be.

“All mortgage lending is done with a tier of interest rates and terms based on consumer credit scores,” Harrison says. “A credit score of 720 or above will earn you the best rates and can potentially save you thousands of dollars.”

A score of 680 to 720 can get you good mortgage rates, while a FICO score of 620 is usually about the lowest score to qualify for most loans, Harrison says.

Consumers should learn about credit scores the minute they start working, Harrison says.

Websites such as Bankrate provide information about how to improve your credit score.

Even after a mortgage approval, consumers must avoid applying for new credit or taking on new debt, Adamo says, because a second credit check is often required before settlement.

First-time homebuyers today typically opt for a 30-year fixed-rate mortgage. Their conservatism is a reaction to stories about the dangers of interest-only mortgages and adjustable-rate mortgages.

But Harrison says home loan alternatives to a 30-year-fixed sometimes make more sense. For example, buyers certain they will be relocated by their companies within five years may find a 5/1 ARM “could be a much better mortgage,” he says.

“There’s no reason to pay a premium for a product you don’t need like a 30-year loan,” Harrison says.

Homebuyers eager to build equity in their homes or who are older and want to live mortgage-free in retirement should consider a 15-year fixed-rate loan or, if they can afford it, even a 10-year mortgage to reach their goals.

Read more: http://www.bankrate.com/finance/real-estate/4-big-money-mistakes-of-first-time-homebuyers-1.aspx

– GATED 15 ACRE LAKEFRONT ESTATE | LUXURY HOME.

View a photo tour on www.LuxuryPortfolio.com

Call to schedule your private tour of this Luxury Estate

Christy Oetken

208-660-0506